ISO 20022 is not a format change. It’s a data shock.

ISO 20022 is not a format change. It’s a data shock.

December 1st, 2025

ISO 20022 is delivered. Understanding comes next.

For years, ISO 20022 was described as a technical migration. An upgrade. A schema change. A regulatory mandate. Now a major milestone has finally been reached.

On 22 November 2025, the coexistence period ended for the major cross-border MT payment messages (MT 103, MT 202 and others), and the industry switched fully to ISO 20022 for FI-to-FI cross-border payments.

Banks upgraded payment engines, implemented MT-to-MX mappings, validated schemas, expanded pipelines and rebuilt data stores so that the richer ISO structure could flow end to end.

These investments were not optional. They were the foundations for everything that is now finally possible.

But they also created something new: pressure.

Banks are now expected to deliver ROI with ISO 20022.

Shareholders expect it. Regulators expect it. Internal sponsors expect it

ISO 20022 is not a format update. It is a data shock. It introduces a structural shift in how payments are described, linked and understood. For the first time, every transaction carries consistent meaning. The migration delivered the data. The value now waits to be unlocked.

And at the same time, organizations feel a second pressure:

Banks are now expected to deliver ROI with AI

Right now, both ISO 20022 and enterprise AI share the same bottleneck: banks have structure but not interpretation, and AI cannot create intelligence on top of unaligned data. ISO 20022 solves the structure problem. A reasoning layer solves the interpretation problem.

ISO 20022 gives structure. AI gives intelligence.

A reasoning layer connect the two.

The urgency is here.

1. ISO 20022 Reshapes What a Payment Is

ISO 20022 introduces three elements previous formats like MT never provided:

- It adds fine-grained structure.

- It adds semantics.

- All this consistently.

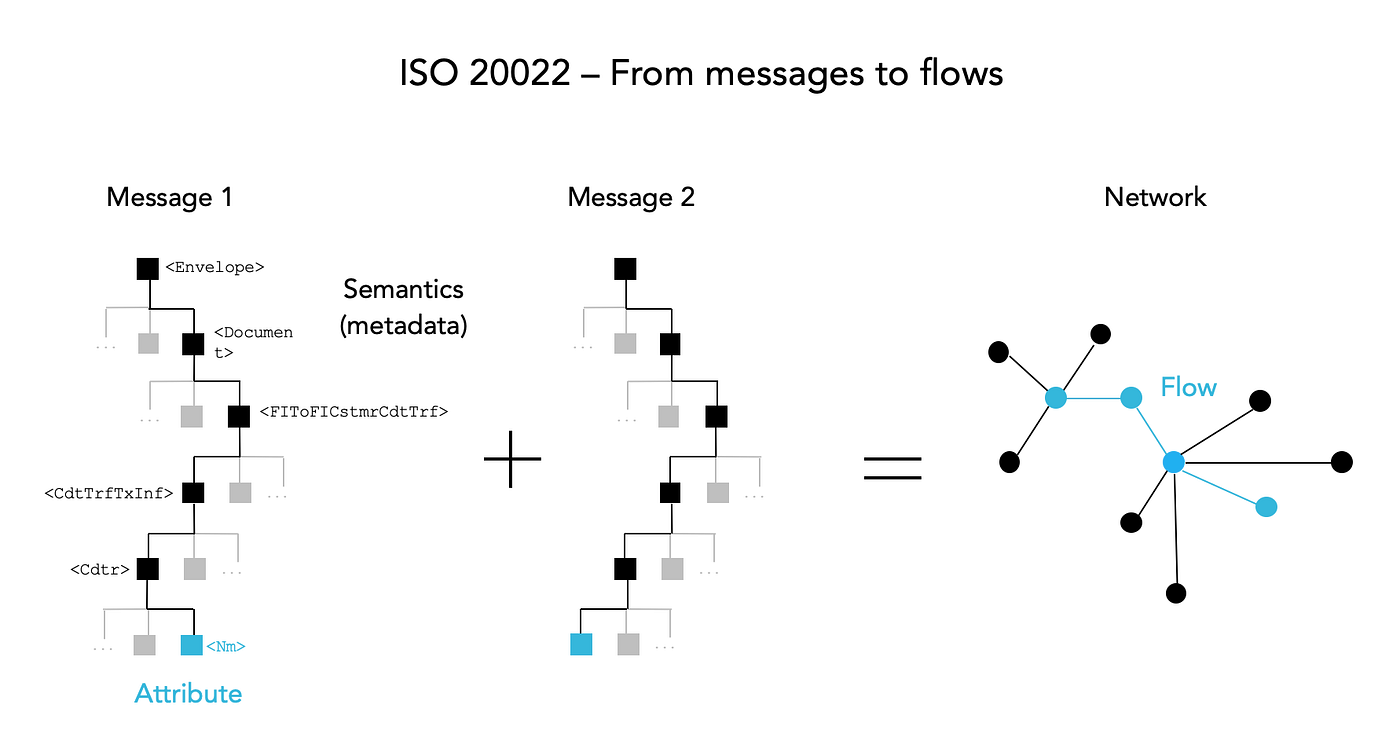

The essential contribution is not only the presence of more fields. ISO 20022 represents a consistent ontology of payments.

A payment is no longer a flat row of attributes. It is a contextualized set of:

- Entities: roles, parties, accounts, identifiers

- Locations and references: structured addresses, remittance details, regulatory tags

- Flow and lifecycle: dates, lifecycle events, cross-referenced message chains

All defined within one coherent model.

Even with minimal population, each transaction sits inside a richer semantic context than anything the MT world provided. The shift is not the volume of data, but the meaning attached to it.

This can unlock automation, analytics, interpretation and AI. But none of this happens automatically. XML messages that sleep in a database do not generate insight. Value appears only when the ontology is interpreted and connected. ISO 20022 expands context faster than today’s tools or mental models can absorb.

It multiplies the data long before it multiplies the understanding.

Meanwhile, AI remains stuck in proofs of concept across the industry. The data fed to LLMs and Agents lacks a consistent and usable structure across use cases, business units and systems. ISO 20022 is quietly solving that problem. What banks now need is the layer that makes this new structure usable.

2. Semantic Complexity. The Unspoken Challenge

Most banks can already store ISO 20022.

- They send/receive it in gateways.

- They can validate schemas.

- They can process rules on top: to route, to screen, to settle, to report

Very few, however, can reason across it.

ISO 20022 is not a format. It is an ontology.

Ontologies are complex by design. A single message type such as pacs.008 can include [1]:

- More than 1,000 attributes

- Hundreds of sub-elements per category

- Nested structures describing roles and parties

- Identifiers reused to connect message chains

- Date types with different meanings

- Roles whose meaning varies by scheme or jurisdiction

This is not a set of columns. It is a semantic model that defines how payment concepts relate to each other.

Human-readable definitions exist, but machines cannot use them directly. Turning definitions into machine logic requires interpretation. It is manual, slow and impossible to scale. Complexity increases further across schemes, rails and jurisdictions.

Storing messages is easy. Understanding them at scale is not. This is the unspoken challenge behind the standard. It is also the reason AI struggles to run and scale reliably on fragmented enterprise data.

Banks have structured messages but not structured meaning.

3. Why Existing Tools Do Not Bridge the Gap

Banks built the foundations for ISO 20022:

- The messages flow.

- The schemas get validated.

- The transactional pipelines run.

- Payments settle.

- Operations continue.

What is missing is interpretation. Tools designed for MT cannot interpret an ontology.

BI tools flatten or ignore the ontology

They collapse semantics into custom columns, store rich elements as text, and can’t create data networks efficiently. The data is present, but the meaning is lost.

Rules engines expect stability

ISO 20022 is intentionally variable. Variation is normal but rules break when structures evolve.

Generic AI and RAG systems cannot interpret ISO 20022

Because of two reasons

- They do not understand the ontology — ignoring lifecycle logic and role semantics, treating ISO 20022 as text, not meaning.

- They cannot ingest millions of transactions as bulk context, not even in RAG mode.

This is why AI in banks is still stuck in pilots, demos and innovation labs. AI cannot generate ROI if it cannot understand the underlying data.

The gap is structural. ISO 20022 encodes meaning but most tools still process formats.

The value is there, but out of reach until banks can interpret the model.

4. Enter the Reasoning Layer

The ISO 20022 ontology is present in every payment. What is missing is the ability to use it. A reasoning layer is the natural next step once an industry standardises its meaning.

- It understands semantics, not syntax.

- It reconstructs flows, not rows.

- It enables AI to reason, not guess.

A reasoning layer must be able to:

- Reconstruct lifecycle chains

- Link messages that matter within a scope of interest

- Interpret roles, parties, identifiers and dates

- Recognize counterparties and behavioral patterns

- Surface anomalies and friction points

- Map flows across corridors and jurisdictions

- Detect unusual behavior across accounts or parties

- Provide a unified view of how transactions move

- Answer business questions in natural language

- Return traceable, auditable results

None of this requires new data. It uses what is already stored.

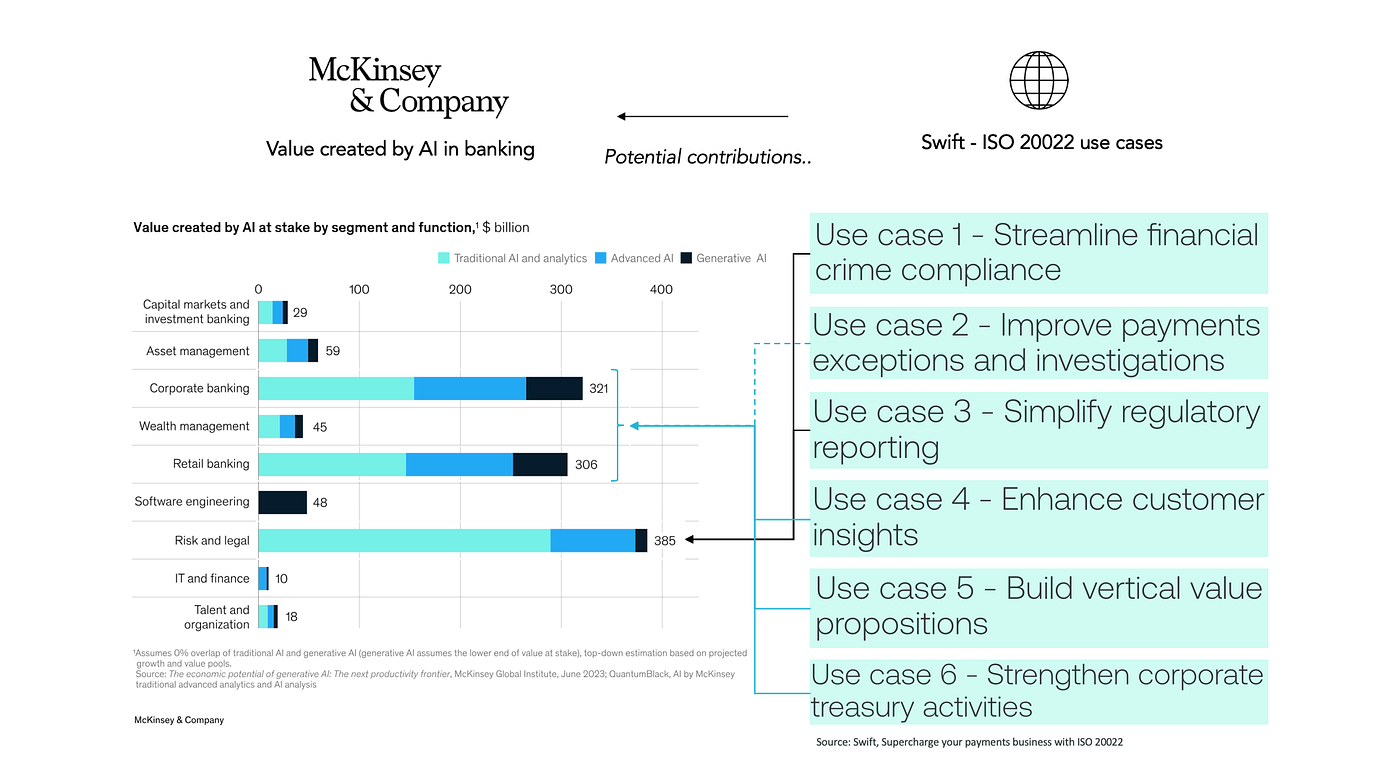

5. What a Reasoning Layer Makes Possible

A reasoning layer does not introduce new information. It reveals what ISO 20022 already describes.

AML and Sanctions

Flow intelligence strengthens AML by showing how money actually moves.

- Expose hidden networks and routing patterns

- Combine roles, behavior and geography into a single, lower-noise risk signal

- Accelerate investigations with pre-assembled context and explainable rationale

ISO 20022 becomes operational AML insight. Noise decreases. Decisions improve.

Cash and Liquidity

Flow intelligence turns liquidity into real-time visibility of how funds move and where risks emerge. Institutions can see:

- Corridor-driven inflows and outflows

- Stability and volatility of flows

- Behaviour across counterparties

- Intraday seasonality and funding peaks

- Settlement frictions and operational bottlenecks

- Early signals of liquidity and counterparty risk

Liquidity shifts from reactive reporting to proactive control.

Client and Counterparty Intelligence

Flow intelligence turns raw activity into relationship insight. ISO 20022 provides a factual basis to observe:

- Who sends what, when and to whom, and why

- How corridors change over time

- Behavioural shifts linked to preferences, operational or market events

- Counterparty concentration and risk

This reveals client patterns MT could never show.

Payments Operations

Operations teams gain a consistent view of the full payment chain. Analysts can ask:

- Fnd all payments returned by a specific institution

- Show the complete licefycle of a transaction

- Identify whether a failure was caused by missing data or regulatory rules

No more stitching systems manually. Root-cause analysis accelerates. Visibility improves.

ISO 20022 makes all these capabilities possible, but only when its semantic relationships are interpreted. A reasoning layer does not create new value. It reveals value already present.

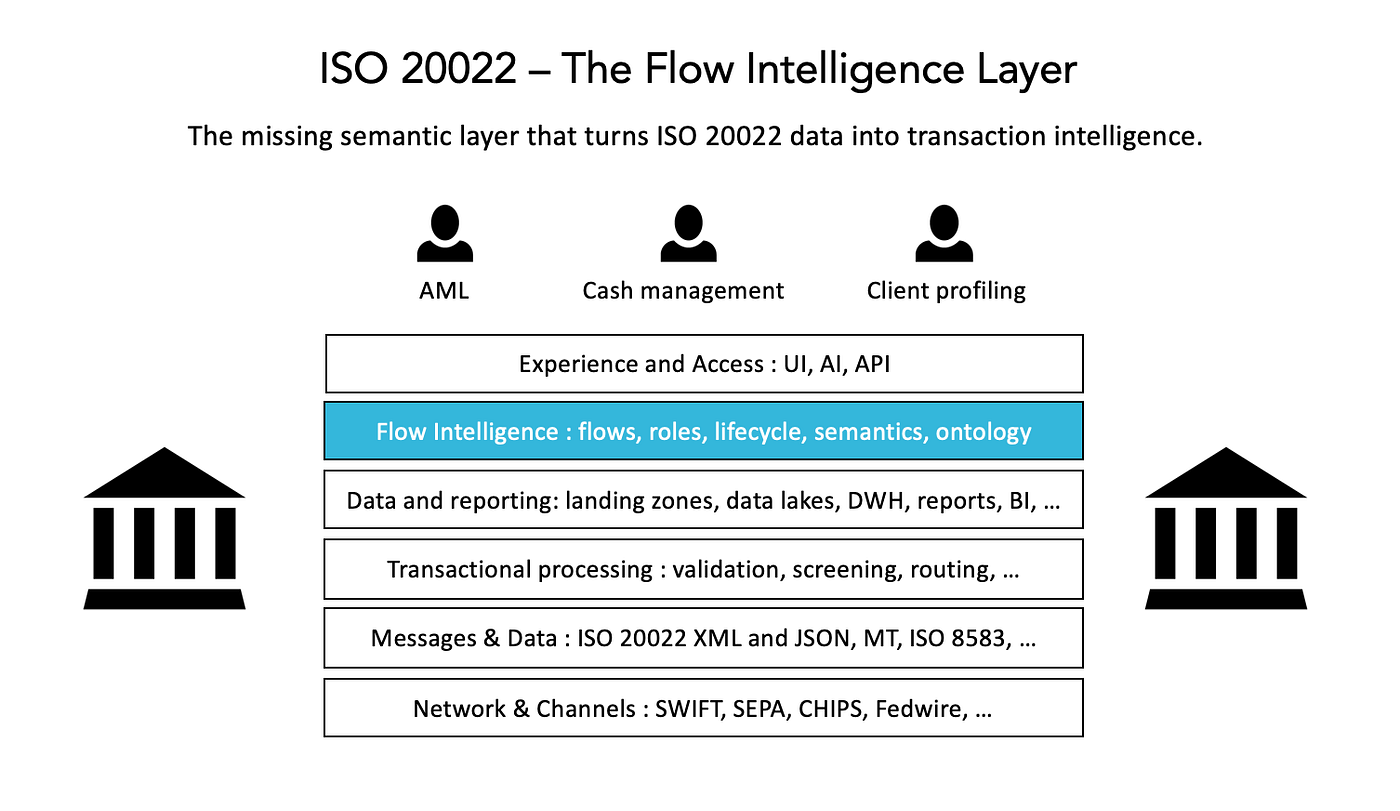

6. Alpina’s Contribution

Banks have completed a hard piece of migration. The structure is there.

What is missing is the interpretive layer. Alpina provides that layer.

We turn ISO 20022 structure into operational intelligence.

TxFlow

TxFlow is the data foundation of the Flow Intelligence Layer. It transforms raw messages into:

- A graph view connecting messages, roles, parties and lifecycle events

- An analytics branch — not interfering transactional core — that remains faithful to the semantic model

TxFlow creates a unified understanding of payment flows across channels and processes.

TxAgent

TxAgent is an ISO 20022 aware reasoning AI agent that:

- Understands the ontology of payments

- Answers business questions in natural language

- Produces traceable and audit-ready results

- Runs entirely inside the bank perimeter

TxAgent uses the data banks already store. It does not replace existing systems. It makes them intelligent.

The Flow Intelligence Layer

TxFlow and TxAgent together form a Flow Intelligence Layer. It does not introduce new infrastructure. It activates the structure already present in ISO 20022.

Institutions gain faster decisions, clearer insight and higher returns from the investments they have already made.

Why Alpina now ?

Because banks need ROI on two fronts at the same time:

- ROI on ISO 20022 investments

- ROI on AI investments

Both converge to the same : a flow intelligence layer. This is precisely what Alpina builds.

Alpina does not solve a side problem. It solves the bottleneck that keeps both ISO and AI from producing value.

7. The Real Migration Starts Now

ISO 20022 is now universal. The coexistence phase is over, the ontology is in place, and every payment carries meaning that MT could never express. The question is no longer whether the migration worked. It did. The question is what institutions will do with the structure they have just built.

Some will treat ISO 20022 as a more detailed MT. Systems will run, operations will stabilise, and the new data will sleep. AI will remain stuck in proofs of concept.

Others will activate the semantics embedded in every message. A reasoning layer is not another project. It is the missing layer in a system that has standardised its language. Without it, the industry has structure but no interpretation.

The next era begins when banks turn ISO 20022 into intelligence and unlock the value already present inside every flow.

ISO 20022 is delivered. Understanding comes next.

References

[1] https://medium.com/@pierre.oberholzer/iso-20022-road-to-riches-4618e029dbf8

[2] https://alpina-analytics.com/iso-20022-ai-transforming-banking/